Understanding First-Time Buyer Loans and Your Options

Stepping into the real estate market is an exciting milestone, but navigating the world of home financing can feel overwhelming. Securing the right first time homebuyer mortgage is the foundation of a successful home purchase. At Convoy Home Loans in California, our mission is to provide future homeowners with financing options that perfectly match their financial goals. Whether you are exploring standard conventional loans or an FHA purchase loan, understanding your choices is critical.

A first-time home buyer mortgage is specifically designed to help new buyers overcome common hurdles like large down payments and strict credit requirements. By exploring dedicated First-Time Buyer Loans, you can unlock flexible terms and competitive rates. Furthermore, if you already have an offer from another lender, we are experts at providing second opinions on first-time homebuyer mortgages to ensure you are truly getting the best deal possible.

Comprehensive Coverage of HomeReady and Home Possible

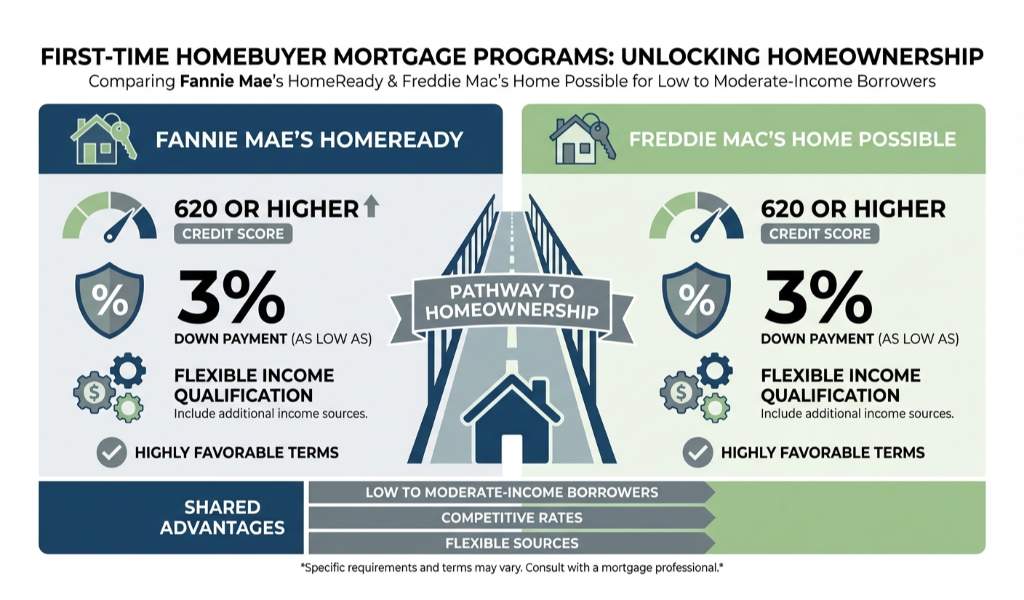

When looking for a first time homebuyer mortgage, two of the most popular and advantageous conventional loan programs are Fannie Mae's HomeReady and Freddie Mac's Home Possible. Both programs are designed to help low to moderate-income borrowers achieve homeownership with highly favorable terms.

-

HomeReady: Ideal for buyers with a credit score of 620 or higher, this program allows for a down payment as low as 3 percent. It also offers flexible income qualification, meaning you can include income from non-borrowing household members.

-

Home Possible: Very similar to HomeReady, this Freddie Mac program also requires just a 3 percent down payment and is structured to assist very low to low-income borrowers. It provides reduced mortgage insurance premiums, which helps keep your monthly payments affordable.

Both of these programs can often be paired with down payment assistance programs to further reduce your out-of-pocket expenses at closing.

|

Feature |

HomeReady (Fannie Mae) |

Home Possible (Freddie Mac) |

|---|---|---|

|

Minimum Down Payment |

3% |

3% |

|

Minimum Credit Score |

Typically 620 |

Typically 660 |

|

Income Limits |

Up to 80% of Area Median Income (AMI) |

Up to 80% of Area Median Income (AMI) |

|

Mortgage Insurance |

Reduced rates, cancelable at 20% equity |

Reduced rates, cancelable at 20% equity |

Why You Need a Second Opinion on Your First-Time Homebuyer Mortgage

Many buyers accept the very first loan offer they receive, potentially leaving thousands of dollars on the table. We are experts at providing second opinions on first-time homebuyer mortgages. Dustin Rosenberg, Jonathan Yoo, and the entire team at Convoy Home Loans pride themselves on treating clients like family. If you have a quote from a retail bank or an online lender, let our team review it. As a fully licensed mortgage broker (NMLS #2130517), we have access to wholesale rates and creative financing options that big banks simply cannot offer.

Getting a second opinion is fast, free, and could dramatically lower your monthly payments. We will patiently educate you on all your First-Time Buyer Loans, ensuring you feel confident and secure in your investment.

Q1: What qualifies as a first time homebuyer mortgage?

A first-time homebuyer mortgage is a loan product designed for individuals who have not owned a principal residence in the past three years. These loans typically feature lower down payment requirements and more flexible credit guidelines.

Q2: What is the difference between HomeReady and an FHA purchase loan?

HomeReady is a conventional loan that requires a minimum 3 percent down payment and allows you to cancel mortgage insurance once you reach 20 percent equity. An FHA loan requires 3.5 percent down, has more lenient credit score requirements, but usually requires mortgage insurance for the life of the loan.

Q3: Can I use down payment assistance programs with First-Time Buyer Loans?

Yes, many First-Time Buyer Loans, including HomeReady, Home Possible, and FHA loans, can be combined with local and state down payment assistance programs to help cover your upfront costs.

Q4: Why should I get a second opinion on my mortgage offer?

Interest rates and lender fees vary significantly between companies. Getting a second opinion ensures you are not being overcharged. At Convoy Home Loans, we frequently beat competitor rates and save our clients money over the life of their loan.

Q5: How do I start the mortgage process in California?

Starting the process is easy. You can reach out to our team at Convoy Home Loans for a free consultation. We will review your financial goals, evaluate your credit, and provide you with a pre-approval letter so you can start shopping for your new home.