Understanding the Construction Permanent Loan Process

Building your dream home in California, requires the right financing strategy. A construction to permanent mortgage, also known as a construction permanent loan, offers a streamlined way to fund both the building phase and your long-term financing. Instead of worrying about multiple approvals, this specialized construction loan provides the capital needed to build your home and automatically converts into a standard mortgage once construction is complete.

At Convoy Home Loans, Dustin Rosenberg, Jonathan Yoo, and our entire team are experts at providing second opinions on construction-to-permanent mortgages. Whether you are exploring a bridge swing loan to transition between properties or considering a conventional fixed rate mortgage for your final financing, we help you navigate the complexities of home construction financing.

One-Time Close vs. Two-Time Close Construction Loans

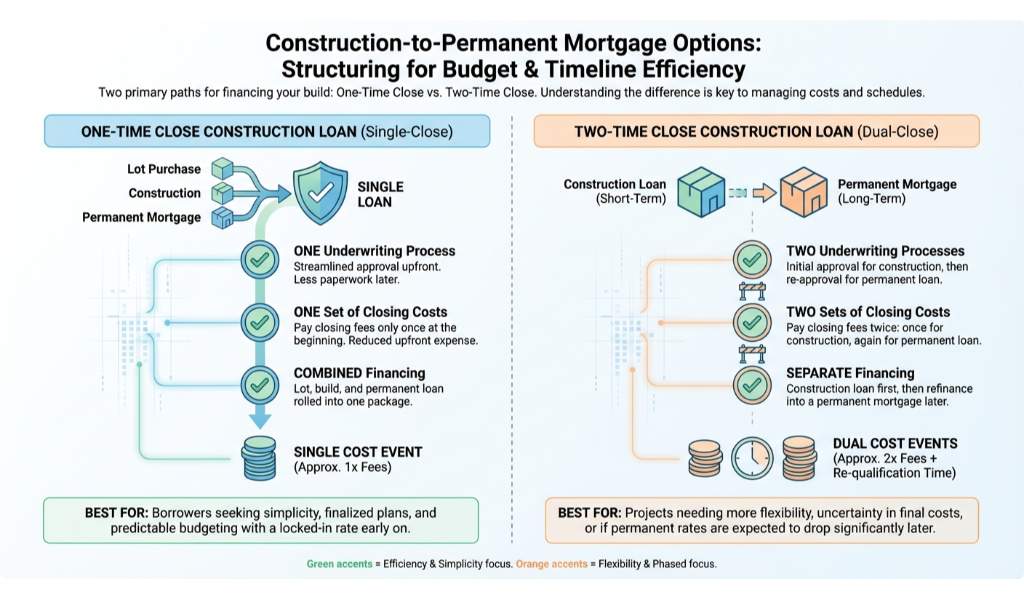

When structuring your construction to permanent mortgage, you generally have two main options: the one-time close and the two-time close. Understanding the difference is crucial for managing your budget and timeline effectively.

-

One-Time Close Construction Loan: This option combines the financing for the lot purchase, construction, and permanent mortgage into a single loan. You only go through the underwriting process once, and you only pay one set of closing costs. It is an excellent choice for borrowers who want a predictable, locked-in interest rate from the start.

-

Two-Time Close Construction Loan: This involves two separate loans. The first is a short-term construction loan to cover the building phase. Once the home is finished, you refinance the debt into a permanent mortgage. While this means paying closing costs twice, it offers more flexibility if you want to shop around for better rates or if your construction costs change significantly.

Choosing the right path depends on your financial goals. If you are unsure which option suits your property, our team at Convoy Home Loans is here to help you weigh the pros and cons.

|

Feature |

One-Time Close |

Two-Time Close |

|---|---|---|

|

Closing Costs |

Paid once |

Paid twice |

|

Interest Rate |

Locked upfront |

Floats until permanent loan |

|

Underwriting |

Single approval process |

Two separate approvals |

|

Flexibility |

Less flexibility to change terms |

High flexibility for final mortgage |

Why Choose Convoy Home Loans for Your Construction Financing

Securing a construction to permanent mortgage requires a lender who understands both the local real estate market and the intricacies of construction financing. As a premier mortgage broker in California, Convoy Home Loans is dedicated to enhancing your standard of living through customized home financing options.

We know that building a home is a massive undertaking. That is why we are experts at providing second opinions on construction-to-permanent mortgages. If you have already received a quote from another lender, let Dustin Rosenberg and Jonathan Yoo review it. We often find opportunities to save our clients money by securing better rates or lower fees.

Convoy Home Loans, Inc. is a fully licensed mortgage broker (NMLS #2130517, DRE #02147305). All information is deemed reliable but not guaranteed and should be independently reviewed and verified.

Q1: What is a construction to permanent mortgage?

It is a financing option that provides funds to build a home and then converts into a permanent mortgage once the construction is completed.

Q2: How does a one-time close construction loan work?

A one-time close loan allows you to secure financing for both the construction phase and the permanent mortgage at the same time, meaning you only pay closing costs once.

Q3: Can I use a construction permanent loan for an investment property?

Yes, depending on the lender and the specific loan product, you can use these loans for primary residences, second homes, and sometimes investment properties.

Q4: What happens if construction takes longer than expected?

Most construction loans have built-in timeframes, typically six to twelve months. If delays occur, you may need to request an extension, which could involve additional fees.

Q5: Why should I get a second opinion on my construction loan?

Getting a second opinion ensures you are getting the most competitive interest rates and terms. At Convoy Home Loans, we specialize in reviewing existing quotes to save you money.