What is a Bank Statement Mortgage?

For many self-employed professionals, freelancers, and small business owners in El Segundo, CA, traditional income verification methods can make securing a home loan challenging. This is where a bank statement mortgage becomes a game-changer. Often referred to as Bank-Statement / Stated-Income Loans, these financing options allow borrowers to qualify for a mortgage using personal or business bank statements instead of traditional W-2s or tax returns.

Traditional lenders typically look at net income after tax write-offs, which may not accurately reflect a business owner's true purchasing power. A bank statement loan focuses on cash flow and deposits to determine your qualifying income. If you have been turned down by another lender, do not worry. We are experts at providing second opinions on bank statement loans and can help you navigate the complexities of a self-employed alternative doc mortgage.

12-Month vs. 24-Month Bank Statements and Alternative Options

When applying for a bank statement mortgage, lenders typically offer options based on the timeline of your financial records. Understanding these variations is crucial for securing the best rate and terms for your Southern California property.

-

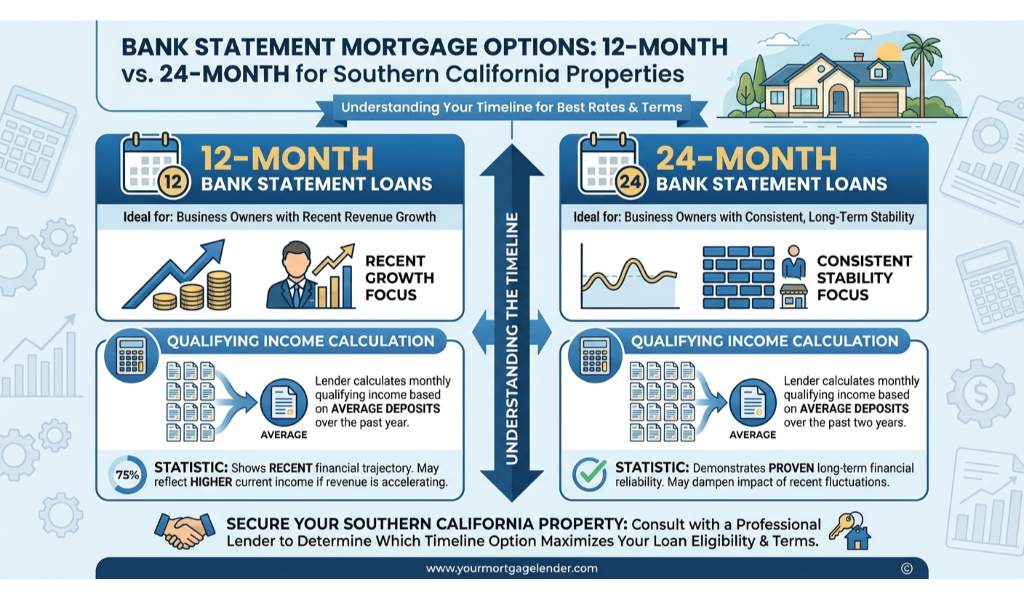

12-Month Bank Statement Loans: Ideal for business owners who have experienced recent revenue growth. The lender calculates your monthly qualifying income based on the average deposits over the past year.

-

24-Month Bank Statement Loans: This option requires two years of statements. It provides the lender with a longer history of consistent cash flow, often resulting in more favorable interest rates.

-

Asset-Based Loans: If you have significant liquid assets but lower monthly cash flow, asset depletion or asset-based loans use your total wealth to calculate qualifying income.

-

DSCR Loans: Real estate investors looking to expand their portfolio can utilize Debt Service Coverage Ratio (DSCR) loans. Instead of personal income, the loan is qualified based on the property's rental income potential.

Because these loans fall outside standard conventional guidelines, they are classified as a non-qualified mortgage (Non-QM). At Convoy Home Loans, we also offer a portfolio in-house underwritten mortgage to provide flexible, common-sense underwriting tailored to your unique financial situation.

|

Loan Type |

Best For |

Income Verification Method |

Typical Focus |

|---|---|---|---|

|

12-Month Bank Statement |

Growing businesses |

Average deposits over 1 year |

Recent cash flow trends |

|

24-Month Bank Statement |

Established businesses |

Average deposits over 2 years |

Long-term income stability |

|

Asset-Based Loan |

High-net-worth borrowers |

Liquid asset depletion |

Total verifiable wealth |

|

DSCR Loan |

Real estate investors |

Property rental income |

Cash flow of the property |

Why Choose Convoy Home Loans for Your Bank Statement Loan?

Securing the right financing requires working with a broker who understands the nuances of alternative documentation. At Convoy Home Loans, our mission is to provide homeowners and future homeowners in El Segundo, CA, and beyond with a variety of home financing options at competitive rates. We treat all our clients like family, taking the time to educate and advise you on your best options.

We are experts at providing second opinions on bank statement loans. If you were told you do not qualify based on your tax returns, let our team review your scenario. We have a track record of beating competitor interest rates and closing fast, ensuring you secure your dream home or investment property without unnecessary stress.

CONVOY HOME LOANS | DRE #02147305 NMLS: #2130517 | Fully Licensed Mortgage Broker. All information is deemed reliable but not guaranteed and should be independently reviewed and verified.

Q1: What is a bank statement mortgage?

A bank statement mortgage is a home loan that allows self-employed borrowers to verify their income using 12 or 24 months of personal or business bank statements instead of traditional tax returns or W-2s.

Q2: Do I need perfect credit for a bank statement loan?

While higher credit scores generally yield better rates, bank statement loans offer flexible underwriting. We can work with various credit profiles to find a solution that fits your specific needs.

Q3: Can I use a bank statement loan for an investment property?

Yes. Bank statement loans can be used for primary residences, second homes, and investment properties. Investors may also consider DSCR loans, which qualify based on the property's rental income rather than personal income.

Q4: What is the difference between a 12-month and 24-month bank statement loan?

A 12-month loan averages your deposits over the last year, which is great for recently growing businesses. A 24-month loan averages deposits over two years, providing lenders with more stability and often resulting in better interest rates.

Q5: Can I get a second opinion if I was denied a mortgage?

Absolutely. We are experts at providing second opinions on bank statement loans. If another lender turned you down due to tax return write-offs, contact us to review your bank statements and cash flow for alternative qualification options.