DSCR vs Conventional Loans: Which One Is Right for Your Investment Property?

Meta description: DSCR vs conventional loans explained. Compare rates, qualification, LLC vesting, and which loan is better for real estate investors in 2026.

If you're buying an investment property, you've probably been pulled in two directions: "Just use a conventional loan, it's cheaper" versus "You need a DSCR loan, it's easier." Both pieces of advice can be right — depending on your situation.

After closing a lot of investment property loans, here's the honest breakdown of when each one wins.

The 30-Second Answer

-

Conventional loan: Best if you have clean W-2 or self-employment income that supports the debt-to-income ratio, you're buying in your personal name, and you haven't hit Fannie Mae's 10-property limit.

-

DSCR loan: Best if your tax returns don't show enough income to qualify, you want to vest in an LLC, you're scaling beyond 10 properties, or you're buying a short-term rental.

Now let's get into the details.

How They Qualify You

This is the single biggest difference.

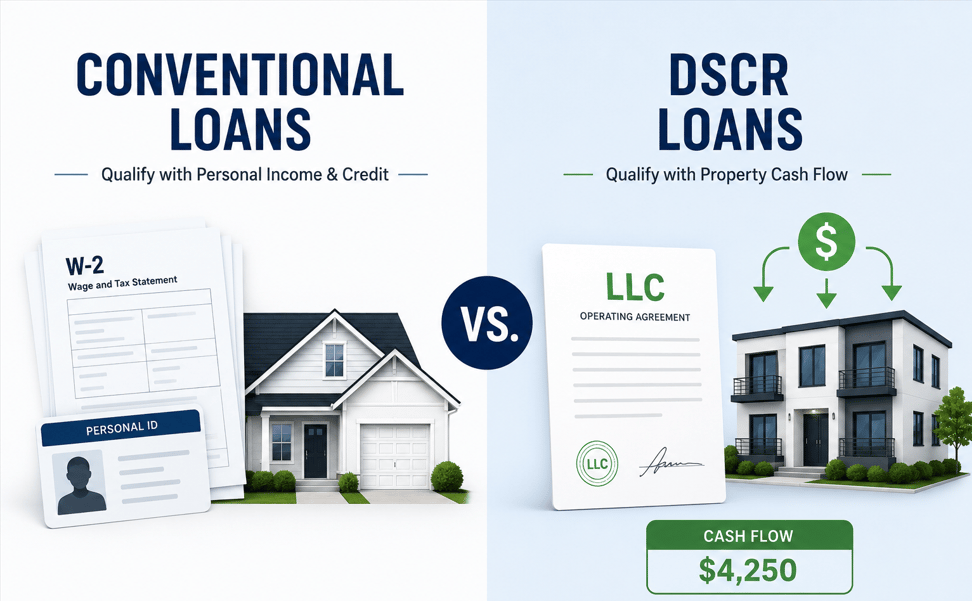

Conventional loans qualify you based on your personal income and debt-to-income (DTI) ratio. The lender wants to see W-2s, tax returns, pay stubs — the works. Your total monthly debts, including the new mortgage, generally can't exceed 43–50% of your gross monthly income.

DSCR loans qualify you based on the property's rental income, not yours. The rent needs to cover the mortgage payment (or close to it). No personal tax returns. No DTI calculation. The property either cash flows or it doesn't.

Here's my favorite way to explain it: DSCR is a creative way to qualify for a loan. Instead of using your personal income, you qualify off only the income the property generates.

A Real Case Study: Why Conventional Killed This Deal

A client of mine — savvy investor, builds wealth the smart way — wanted to buy a 4-unit property in Los Angeles. Strong rents. Solid neighborhood. Numbers worked.

Conventional said no.

Why? Two reasons:

-

He writes off a lot on his taxes (smart move for cash flow, brutal for DTI).

-

He wanted to close in an LLC for asset protection — which conventional doesn't allow.

We closed it as a DSCR loan. No tax returns. LLC vesting. Done.

This is the most common reason investors switch from conventional to DSCR: their tax strategy is working against them at the underwriting desk.

Rates: How Much More Does DSCR Cost?

Here's where conventional usually wins on paper.

Conventional investment property rates are typically the lowest you'll see for a non-owner-occupied loan, because they're backed by Fannie Mae and Freddie Mac.

DSCR rates are slightly higher because they're non-QM (non-qualified mortgage) loans. That said, current pricing is better than most investors realize:

-

As low as the low 5s in certain scenarios

-

Mid-to-low 6s for most deals right now

The spread between conventional and DSCR is often smaller than the time, hassle, and tax-return acrobatics you'd burn trying to force a conventional approval.

Vesting: Personal Name vs. LLC

-

Conventional: Personal name only. You cannot close a conventional loan in an LLC. Period.

-

DSCR: LLC, personal name, or trust. Your choice.

If you're serious about scaling a rental portfolio, asset protection through an LLC is usually non-negotiable. DSCR makes that possible without jumping through hoops.

Property Limits: The 10-Property Cap

Fannie Mae caps you at 10 financed properties total. Once you hit that ceiling, conventional financing is off the table for your 11th deal — even if your income could support it.

DSCR loans have no portfolio limit. You can do your 11th, 20th, or 50th. This is why every serious portfolio investor I know eventually moves to DSCR.

Property Types: What Each Loan Will Touch

Conventional will fund: single-family rentals, 2–4 units (with some restrictions on warrantable condos and unique properties), standard residential investment.

DSCR will fund: single-family rentals, 2–4 units, condos (including non-warrantable), short-term rentals like Airbnb and VRBO, mixed-use properties, and 5+ unit multifamily. Much broader product set.

If you're buying anything unusual — a non-warrantable condo, a vacation rental, a small multifamily — DSCR is usually the path.

Speed to Close

This surprises people: DSCR loans often close faster than conventional, especially for self-employed borrowers.

Why? Less documentation. We're not waiting on tax transcripts from the IRS, chasing P&Ls, or re-verifying income. The property either qualifies or it doesn't.

For experienced investors, that speed matters — especially in competitive markets.

Side-by-Side Comparison

|

Feature |

Conventional |

DSCR |

|---|---|---|

|

Qualification |

Personal income/DTI |

Property rental income |

|

Tax returns required? |

Yes |

No |

|

LLC vesting allowed? |

No |

Yes |

|

Max financed properties |

10 |

Unlimited |

|

Short-term rentals |

Limited |

Yes |

|

Typical rate (2026) |

Lowest |

Slightly higher (low 5s–mid 6s) |

|

Speed to close |

Slower |

Faster |

|

Best for |

W-2 borrowers, clean DTI |

Investors, LLC vesting, scaling |

So Which One Should You Choose?

Be honest with yourself:

Go conventional if you have clean W-2 income, you're fine vesting personally, you're under 10 financed properties, and you want the absolute lowest rate.

Go DSCR if your tax returns understate your real income, you want LLC vesting, you're scaling past 10 properties, you're buying a short-term rental, or you just want a smoother close.

There's no shame in either. The smartest investors I work with use both — conventional for the easier W-2-friendly deals, DSCR for everything else.

Not Sure Which Is Right for Your Deal?

This isn't a decision to guess at. The wrong loan can cost you tens of thousands over the life of the property, or worse — kill the deal entirely.

We're a mortgage brokerage with access to multiple wholesale lenders on both the conventional and DSCR side. We'll run your scenario through both and tell you straight up which one makes sense.

Call us at 800-913-2169.

Ten minutes on the phone can save you a lot of headaches.

Convoy Home Loans is a nationwide mortgage brokerage specializing in investment property financing. Rates and program guidelines subject to change.